Thinking About Using Your 401(k) To Buy a Home?

Are you dreaming of buying your own home and wondering about how you’ll save for a down payment? You’re not alone. Some people think about tapping into their 401(k) savings to make it happen. But before you decide to dip into your retirement to buy a home, be sure to consider all possible alternatives and talk with a financial expert. Here’s why.

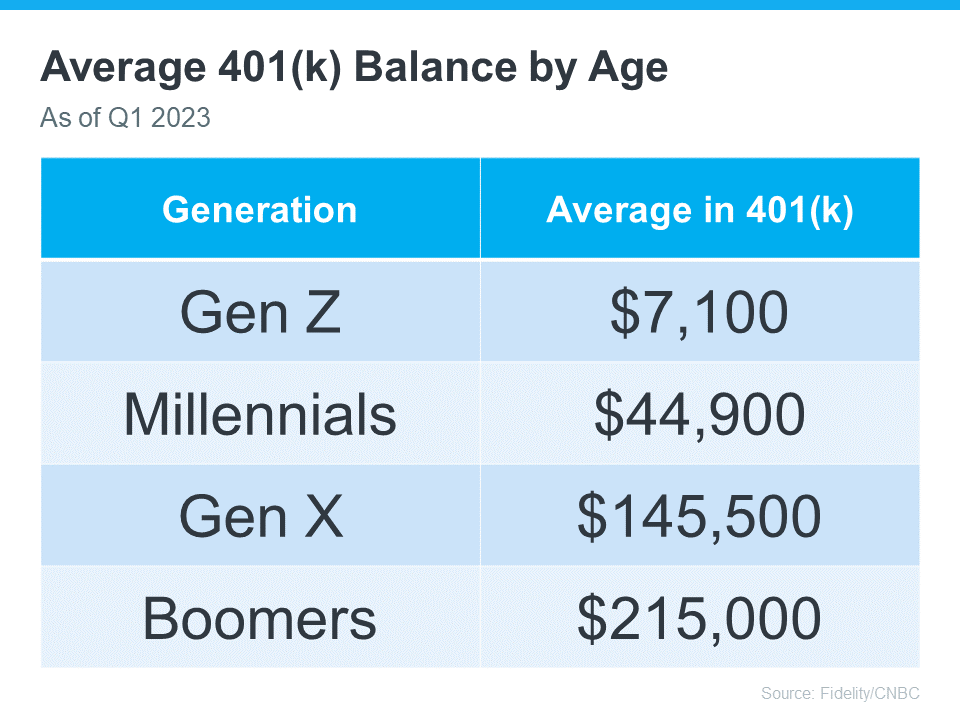

The Numbers May Make It Tempting

The data shows many Americans have saved a considerable amount for retirement (see chart below):

It can be really tempting when you have a lot of money saved up in your 401(k) and you see your dream home on the horizon. But remember, dipping into your retirement savings for a home could cost you a penalty and affect your finances later on. That’s why it’s important to explore all your options when it comes to saving for a down payment and buying a home. As Experian says:

“It’s possible to use funds from your 401(k) to buy a house, but whether you should depends on several factors, including taxes and penalties, how much you’ve already saved and your unique financial circumstances.”

Alternative Ways To Buy a Home

Using your 401(k) is one way to finance a home, but it’s not the only option. Before you decide, consider a couple of other methods, courtesy of Experian:

- FHA Loan: FHA loans allow qualified buyers to put down as little as 3.5% of the home’s price, depending on their credit scores.

- Down Payment Assistance Programs: There are many national and local programs that can help first-time and repeat homebuyers come up with the necessary down payment.

Above All Else, Have a Plan

No matter what route you take to purchase a home, be sure to talk with a financial expert before you do anything. Working with a team of experts to develop a concrete plan prior to starting your journey to homeownership is the key to success. Kelly Palmer, Founder of The Wealthy Parent, says:

“I have seen parents pausing contributions to their retirement plans in favor of affording a larger home often with the hope they can refinance in the future… As long as there is a tangible plan in place to get back to saving for their retirement goals, I encourage families to consider all their options.”

Bottom Line

If you’re still thinking about using your 401(k)-retirement savings for a home down payment, consider all your options and work with a financial professional before you make any decisions.

Planning to buy? Get your search of homes for sale in Pittsburgh started.

Planning to sell? Download your free home seller’s guide.

Are you relocating to the Pittsburgh area? I can make your move stress-free.

Explore our communities, and then give me a call at (724) 309-1758.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Christa Ross does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Christa Ross will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

![Find Your Dream Home with an Accredited Buyer’s Representative (ABR®) [INFOGRAPHIC]](https://www.bestpittsburghhomes.com/wp-content/uploads/2024/04/dreamhome-500x383.png)

![Buying A Home? 7 Reasons To Hire an Accredited Buyer’s Representative (ABR®) [INFOGRAPHIC]](https://www.bestpittsburghhomes.com/wp-content/uploads/2024/04/7reasons-500x383.png)

![Your Buyer’s Agent Wears Many Hats [INFOGRAPHIC]](https://www.bestpittsburghhomes.com/wp-content/uploads/2024/04/manyhats-500x383.jpg)

![Housing Market Forecast for the Rest of 2023 [INFOGRAPHIC]](https://www.bestpittsburghhomes.com/wp-content/uploads/2023/08/housingmarketforcast-500x383.jpg)

![More Listings Are Coming onto the Market [INFOGRAPHIC]](https://www.bestpittsburghhomes.com/wp-content/uploads/2022/06/Morelistings-500x383.jpg)

![Financial Fundamentals for Homebuyers [INFOGRAPHIC]](https://www.bestpittsburghhomes.com/wp-content/uploads/2021/01/financialfundamental_feature-500x383.jpg)

![The Housing Market Is Positioned to Help the Economy Recover [INFOGRAPHIC]](https://www.bestpittsburghhomes.com/wp-content/uploads/2020/04/housingrecession-500x383.jpg)

![5 Reasons Why Millennials Buy a Home [INFOGRAPHIC]](https://www.bestpittsburghhomes.com/wp-content/uploads/2019/04/Millennials-Choose-to-Buy-ENG-MEM1-1046x1354-500x383.jpg)